You can visit the

complete PDF version

of this document or

an abbreviated version also in PDF.

Cardprofit is an analytics and recommendation application

designed to increase credit card profitability and opportunity discovery for Issuer and

Acquirer portfolios.

CardProfit is an analytics, business intelligence

and strategic recomendation application for the integral administration of payments

portfolios. It is used to increase profitability and opportunity discovery in Issuer

portfolios in multi-dimensional cross-segmented

markets, and to derive unit indicators and profitability benchmarks in order to support

profitability and performance goal setting, valuation and monitoring. It is also used to

promote portfolio product development and performance and facilitate studies of tendencies

and life cycle issues. There is no similar or remotely comparable technology in the market

today, because analytics without profitability extraction and optimization will not address

the customers' bottom line. The CardProfit architecture is highly scalable and is designed

to run in the cloud under elastic servers with massive storage and processing capacity.

With CardProfit, bank-specific market segmentations can be created. For example, the Issuer

business can be segmented by product, brand, product type, geographical regions, cardholder

activity, credit limit usage, consumption volume, etc. CardProfit proposes a paradigm shift

to a competitive emphasis where segmentations can be profiled in terms of unit indicators

so that their performance can be isolated, compared and new opportunities identified. In

particular, cross or intersected segmentations are essencial to the understanding of the roles

played by intersecting, independent market factors in opportunity discovery. For Issuer this

leads to the discovery of opportunities and the realignment, redistribution and redesign of

the product portfolio and cardholder populations based on transactional frequencies, balance

and credit limit usage, etc., all resulting in increases in product performance and profitability.

The CardProfit profitability methodology has been applied extensively and has resulted in

profitability increases between 25% and 50%.

Each variable or unit indicator in the Issuer (or Acquirer) model can be visualized historically

and through time periods of any duration. Notice that the values shown in the following examples

are not realistic because the data has been generated randomly.

1 Issuer

1.1 Increasing Profitability with Benchmarks and Goals

It is not possible to optimize profitability without creating a profitability separation between segments and

between value sources. Without profitabiity unit indicators, it is not possible to compare segments or

their value sources. Unit indicator benchmarks offer a frame of reference

with which to make decisions towards profitability goal setting. External

unit benchmarks, when available, are beneficial but their use limited to average comparisons and not to

profitability optimization. It is considered necessary then for a bank to have the ability to automatically

generate a wide variety or catalog of internal unit benchmarks in order to properly characterize the range and

behavior of the bank's very own business experience.

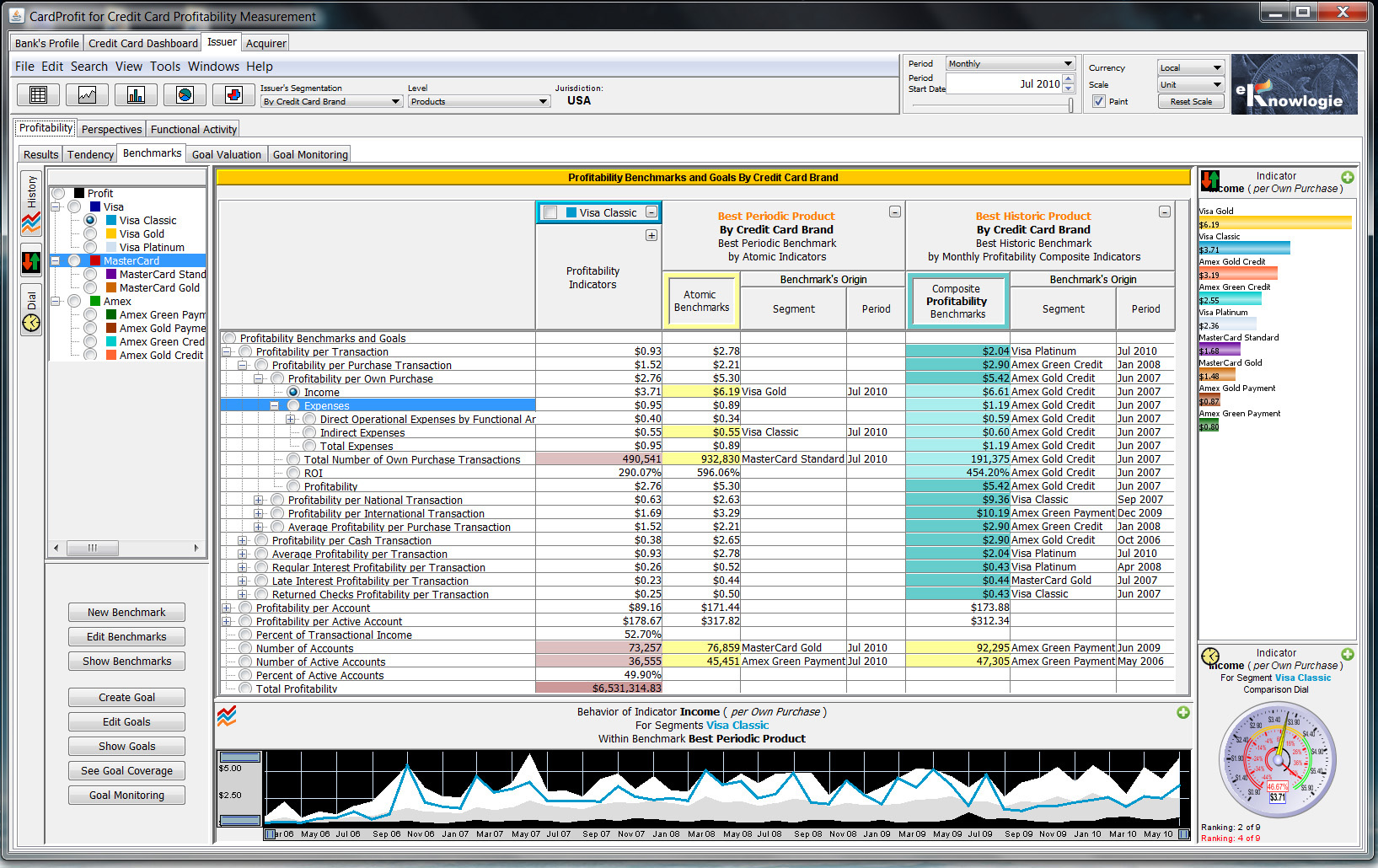

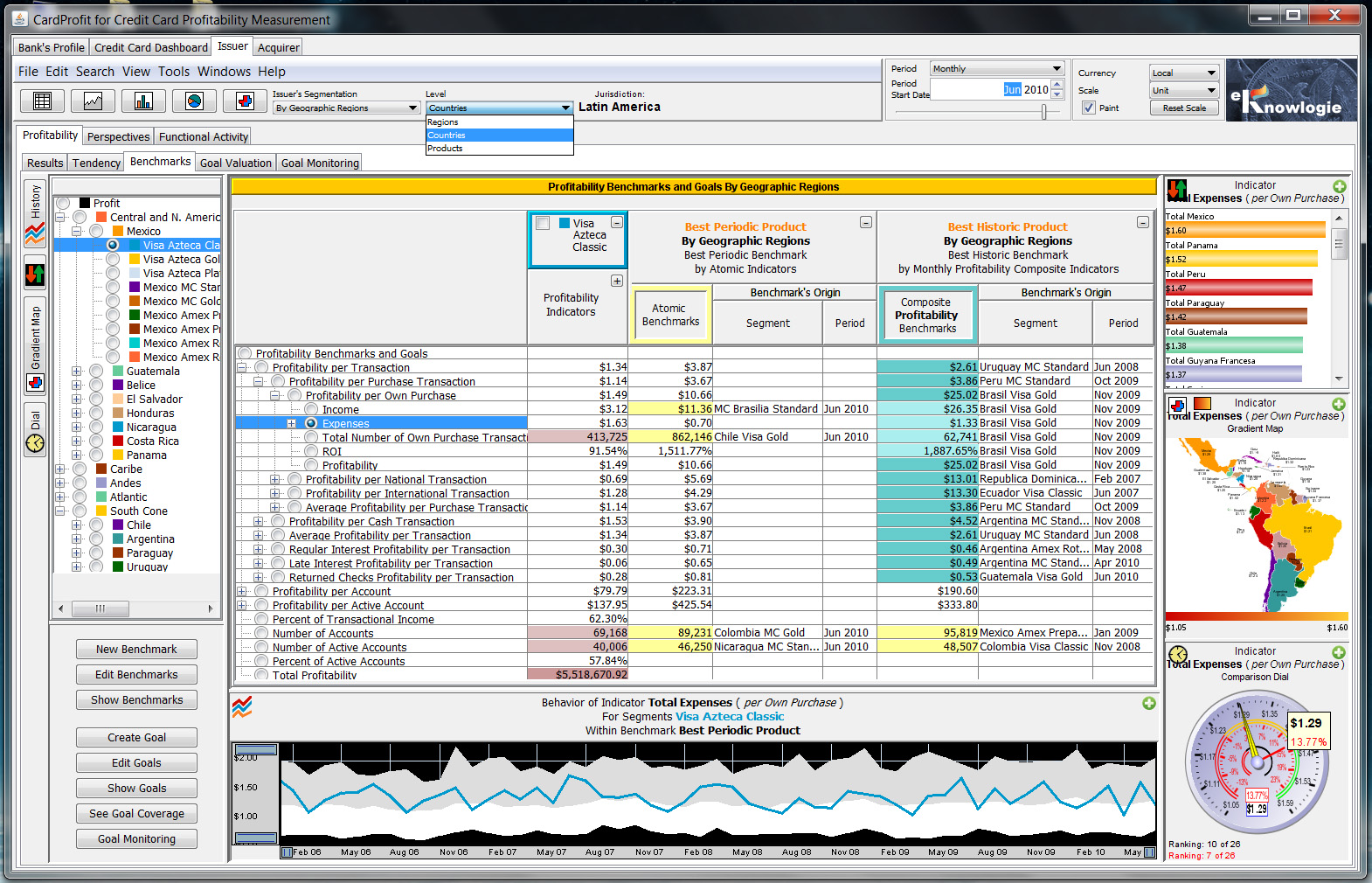

Creation of Unit Benchmarks

The next example shows profitability unit indicators for segment Visa Classic, located within a simple

brand hierarchy. Such panel also shows two of the benchmarks in the bank's catalog, which place Visa Classic

within a frame of reference. The composite indicator benchmarks shown in the table simply refer to indicators

derived from others, such as profitability indicators wich are produced from income minus cost indicators. Any

of the indicators shown in the main table rows can be studied in depth at the hierarchy level selected in the

tool bar. This hierarchy is very simple, with only two levels, Brands and Products, but other

hierarchies may additionally include geographical regions, countries, and newly acquired bank subsidiaries. The

selected Income per Own Purchase indicator is shown in a line chart against a benchmark and in additional bar and dial

chart comparisons with other segments in the level Products. Notice that the values shown in the

following examples are not realistic because the data has been generated randomly.

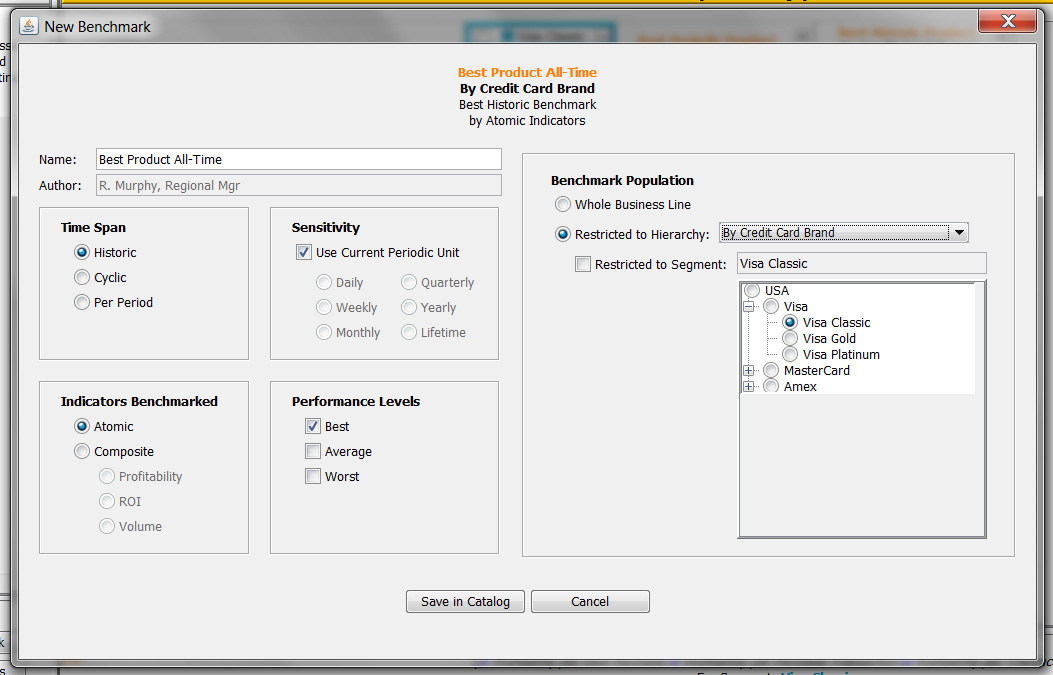

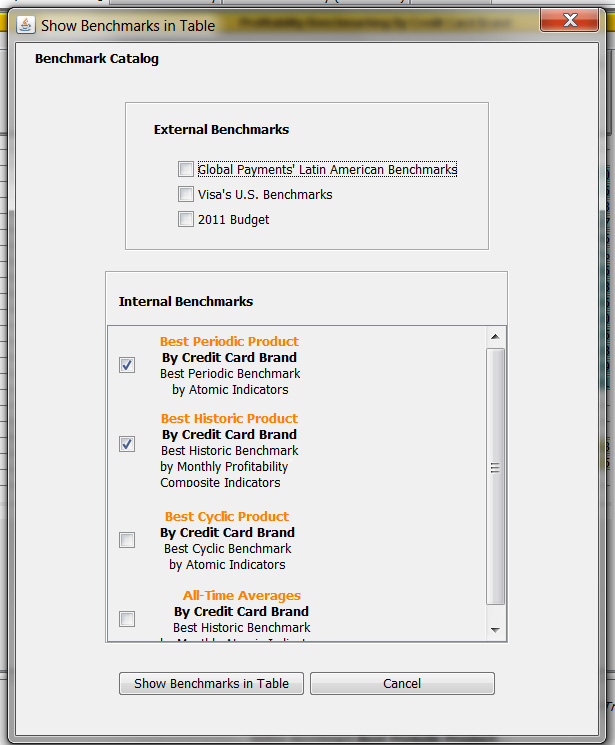

These two panels in the next example show how benchmarks can be created, stored in the bank's catalog,

and visualized in tables and charts, as shown in the previous example. Notice that budgets are also

considered benchmarks.

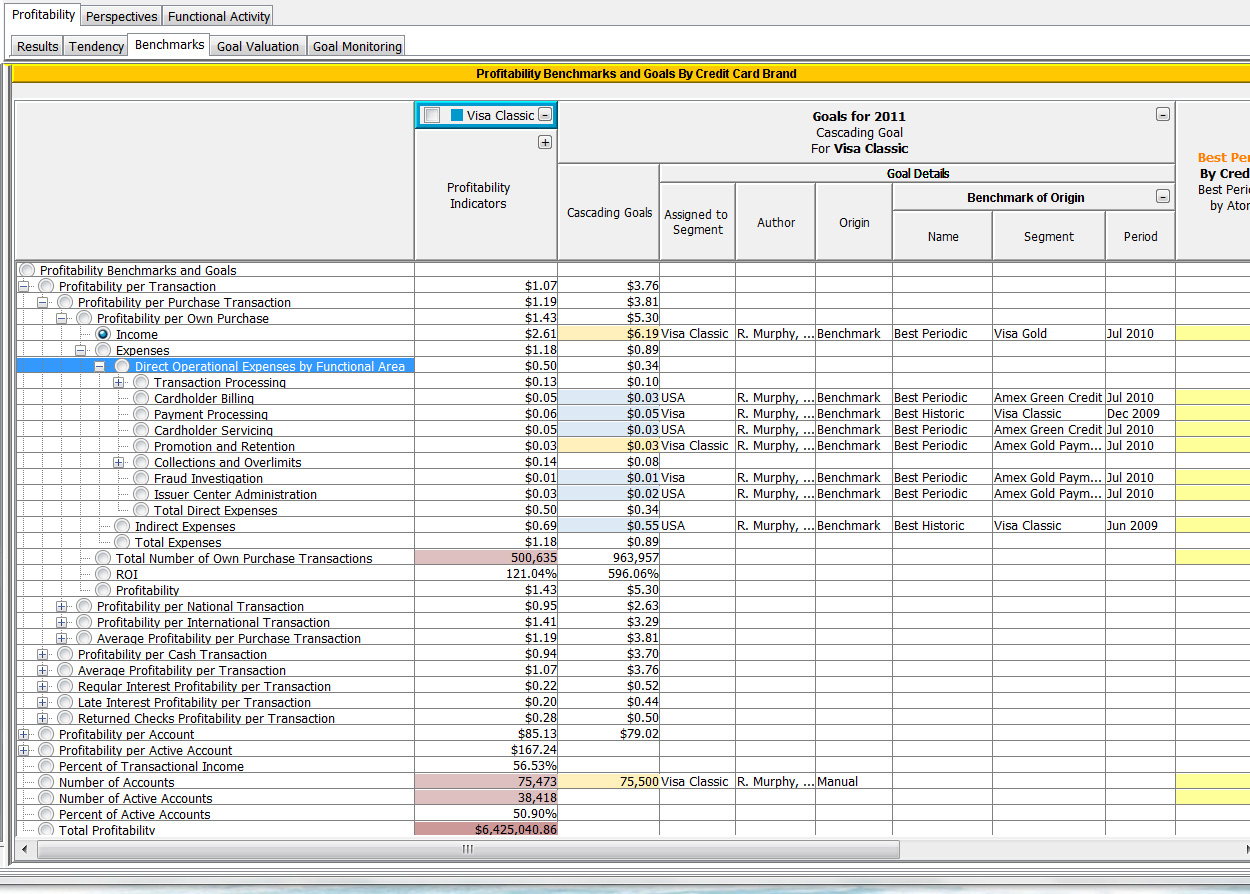

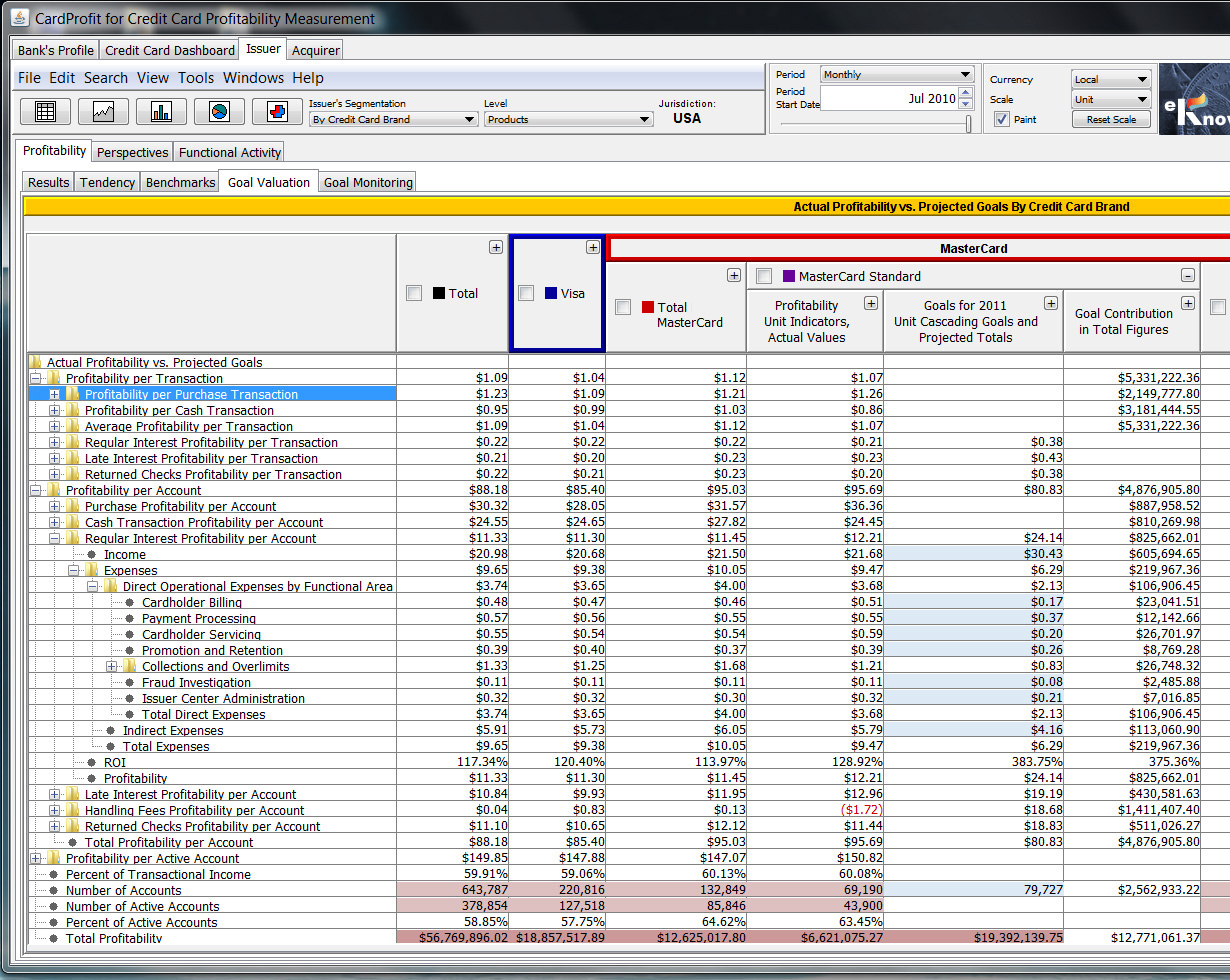

Cascade Goals Setting and Partial Coverage

The next step consists of the establishment of cascading goals for the Issuer business. In the table below

we can see an example of such goal setting. Notice that of all the goals applicable to Visa Classic,

some goals were inherited in cascade from its enclosing group segments, the Visa brand group and the

business root USA (show in light blue), while other goals were assigned specifically to

this segment, Visa Classic (in light orange). We can also observe that some goals come directly from

benchmarks in the catalog, while others (such as Number of Accounts) were created manually. CardProfit

is most flexible in that it is not necessary to "cover" all unit indicators with goals, nor all segments in the

hierarchy. We could for example, establish goals only for processing expenses per transaction, and leave the rest

of the indicators, such as incoming interchange income, regular interest income, other costs, number of transactions

per account, etc., uncovered (without goals). Likewise, "group goals", such as processing expenses per transaction,

can be used to cover more detailed goals, such as processing expenses per own, national and international

transactions. CardProfit was designed to offer full goal valuation and monitoring functionality of partially

covering goals.

Goal Valuation

Once created, these unit goals must be valuated in such a way that for each unit goal we can obtain the total

monetary increase that such goal will represent for each segment to which it was assigned, or conversely,

the total monetary increase of all goals assigned to each segment or segment group. So for example, if we assign

a goal to the unit indicator Processing Expenses per Own Purchase Transaction for a segment representing

an entire geographical region in a multi-national bank (perhaps because we have established that such transaction processing

must from now on be guided by the same standards), we will be able to immediately see the total monetary impact

of such a goal for each product, country and the region as a whole. The example below illustrates the concept

of goal valuation.

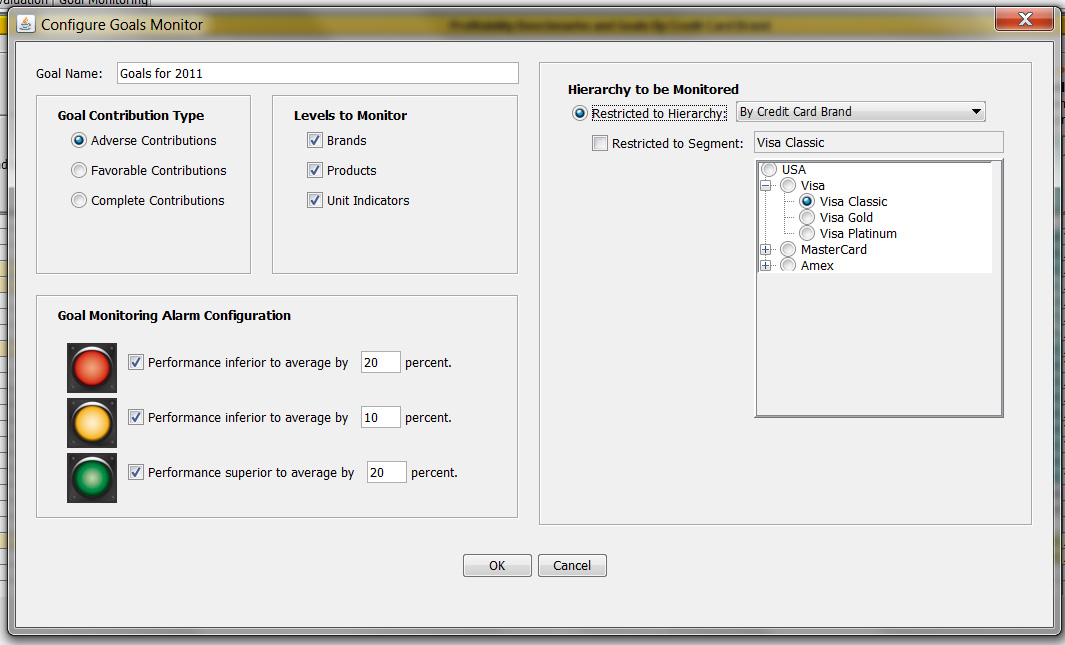

Goal Monitoring

Once these goals have been valuated and approved, these goals' progress must be monitored through the goals'

term, at any level of detail in the segment hierarchy, and for each segment or group. The fact that a given

segment may meet its assigned accumulative goal, is not an implication that its individual unit goals are exempt from

scrutiny, because some unit indicators may be outperforming their goals, thus suggesting a goal

reassessment towards better performance, while others may be drastically underperforming their goals, thus

triggering the necessary functional corrective measures to meet such goals and further improve the segment's

performance. Therefore, it is necessary that goal monitoring includes separate reviews of adverse, favorable and

complete goal contributions for each individual and accumulated goals. The following example shows the process

of goal monitoring configuration.

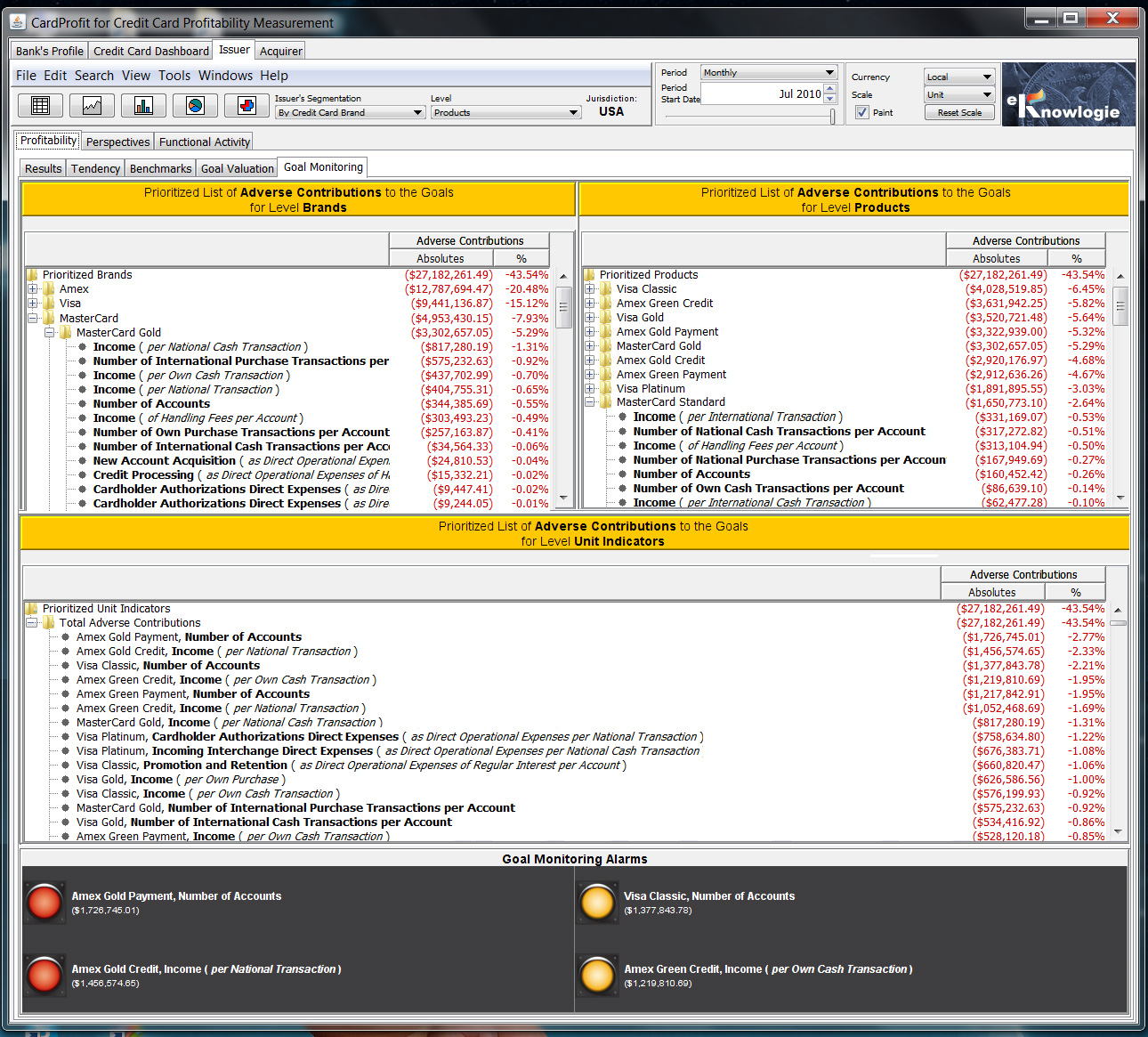

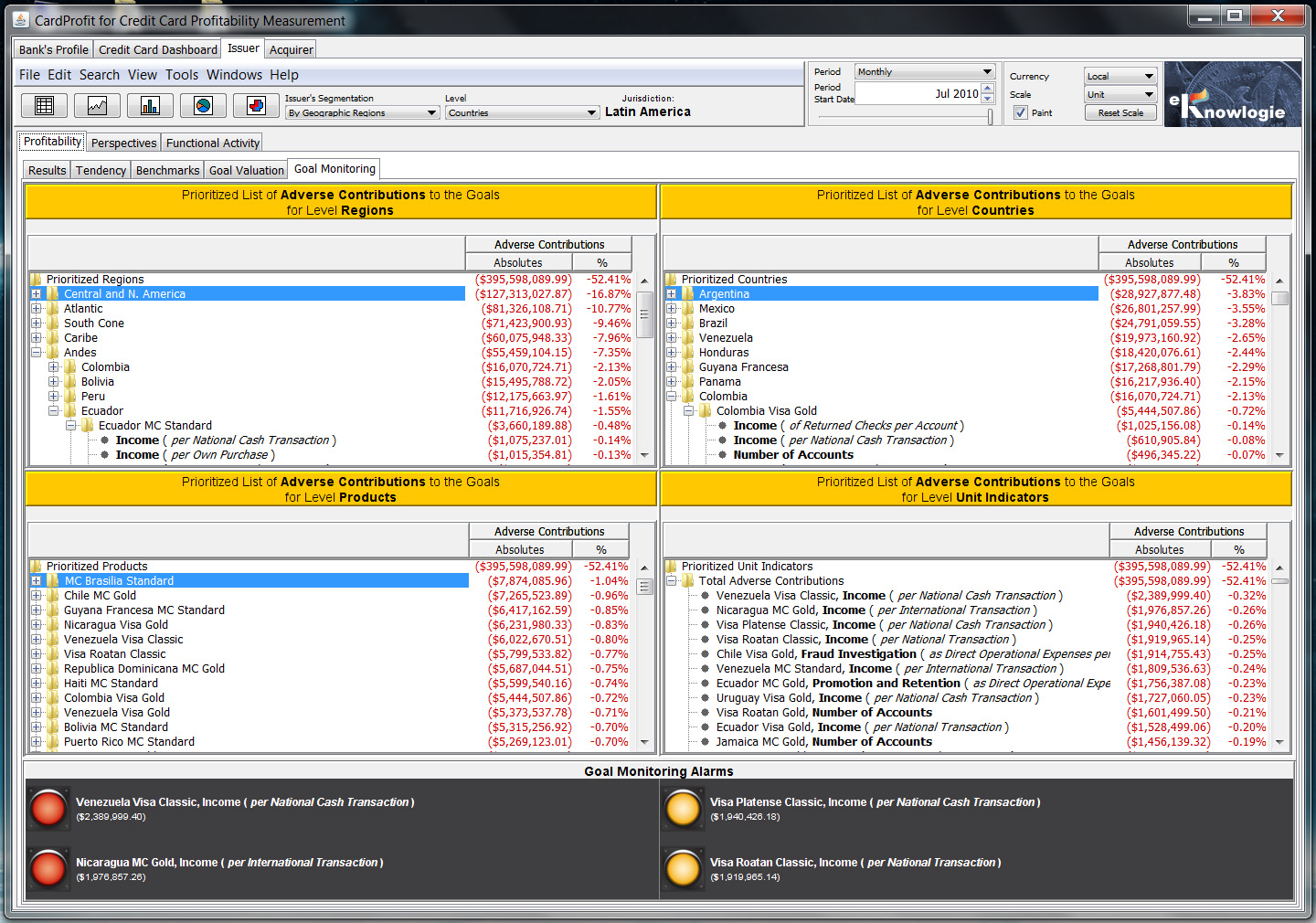

The following example shows goal monitoring for adverse contributions at all levels in the given hierarchy.

These tables are prioritized from high to low adversity and illustrate the need to produce such tables for

each level in the hierarchy. For example, even though the brand with most adverse contributions is Amex,

we can observe that the product with most adverse contributions is Visa Classic, which does not belong

to the most adverse brand. Similarly, the most adverse indicator, Amex Gold Payment, Number of Accounts,

does not belong to the most adverse product. Analysis at each level of detail encourages the use of different

corrective strategies for the management teams at each level, while providing the bank's global management with

a complete X-ray of the entire business.

A simple example of using benchmarks and goals consists of creating a historic average benchmark for all products.

With one click, all unit indicators in this benchmark can be assigned to the root of the product hierarchy, and that's it.

These goals are automatically propagated in cascade to all the products in the hierarchy. Goal progress can then be

monitored by inspecting negative goal deviation reports and alarms for the hierarchy levels, products and indicators

within products. Because we selected an average benchmark, we know that about half of the indicators will have

a performance superior to the benchmark, and thus we are not interested in positive or consolidated (positive plus negative)

deviations. We are interested in having negative deviations (below average) improve to at least the average. If

we use this strategy in consecutive years, the average will improve gradually but significantly.

The example above can be extended by assigning individual goals from different benchmarks which would override

the propagation in cascade of the average benchmark. Comparative studies to understand differences between

segments with best performance according to different benchmarks, would result in the assignment of more insightful

and beneficial goals specific to these segments.

CardProfit offers the concept of jurisdictions. The jurisdiction por each user is the level of

visualization of the model for such user. This way, users can have geographical jurisdictions which

allow each user access only to the model of the country or region relevant to that user, while at the same

time maintaining access to the global indicators and standards automatically generated by CardProfit with the

purpose of establishing anonymous performance comparisons and benchmarking. Global company executives

can of course have full access to the global model. Other jurisdictions of interest include jurisdictions

by product family brand, such that a specific brand jurisdiction could be shared with that brand's

executives, allowing other brands in the model to remain anonymous. This concept of jurisdictions is

extremely useful to multinational banks.

Multi-National Banking

Banks which offer credit card products through their newly-acquired banks or regional or country-based bank subsidiaries

may want to create a segmentation that reflects that organization, such as the one shown in the examples below

for a latin american multi-national bank. Every indicator can still be compared in depth at any of the levels in the

hierarchy for the entire bank (e.g. Regions, Countries, Products).

Goals can still be monitored throughout the entire global structure in the bank, and for all levels in the hierarchy.

Again, notice how the single indicator with the most adverse goal contribution does not belong to the product with

the most adverse contribution, which in turn does not belong to the country or region with the most adverse contribution,

thus emphasizing the need for corrective measures through proper management relationships between the levels in this

hierarchy.

1.2 Profitability Tendency Analysis

The following example shows an Issuer profitability tendency dashboard where the profitability tendencies

can be analyzed in detail.

1.3 Segmented Profitability Results

The following example shows the Income Statement for the Issuer business. The hierarchy in the columns

allows visiting the chosen segmentation at any level of detail. Similarly, the hierarchy in the rows allows

visiting each Income Statement at any level of detail. This allows the use of one given table for executive

strategic purposes as well as for detailed operational purposes. Once again, the values shown in these

examples may not be realistic, simply because the data has been generated at random in order to avoid

any similarities to specific scenarios.

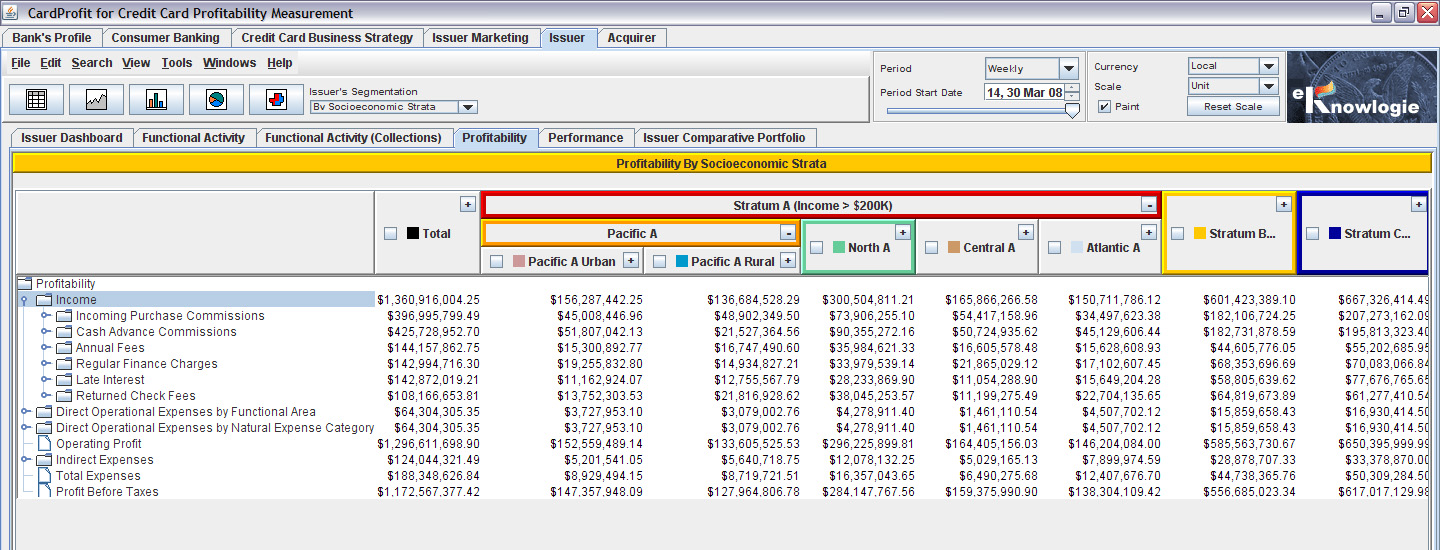

The following example shows the Income Statement for the Issuer business segmented by socioeconomic strata

cross-referenced with geographical regional segments.

1.4 Issuer's Perspectives

A line of business can be managed from different perspectives, where each offers a particular

analytical emphasis. The

main perspective supported is profitability, but other perspectives include marketing, risk-management,

CRM, and operations. CardProfit offers executive perspectives which are consolidated perspectives

across multiple lines of businesses.

CardProfit's multidimensional market segmentation is uniquely suitable for CRM analysis, because it

allows the evaluation of CRM segments from the profitability perspective. CRM tools for the credit card

and payments industry do not support profitability measurement,

rendering them unable to classify segments by their impact on the profitability of the business. This

suggests that market segmentation for profitability measurement and CRM are inseparable, given that in

order to carry out CRM impact studies on the bottom line, it is necessary that such a study be supported

with a profitability and financial performance infrastructure.

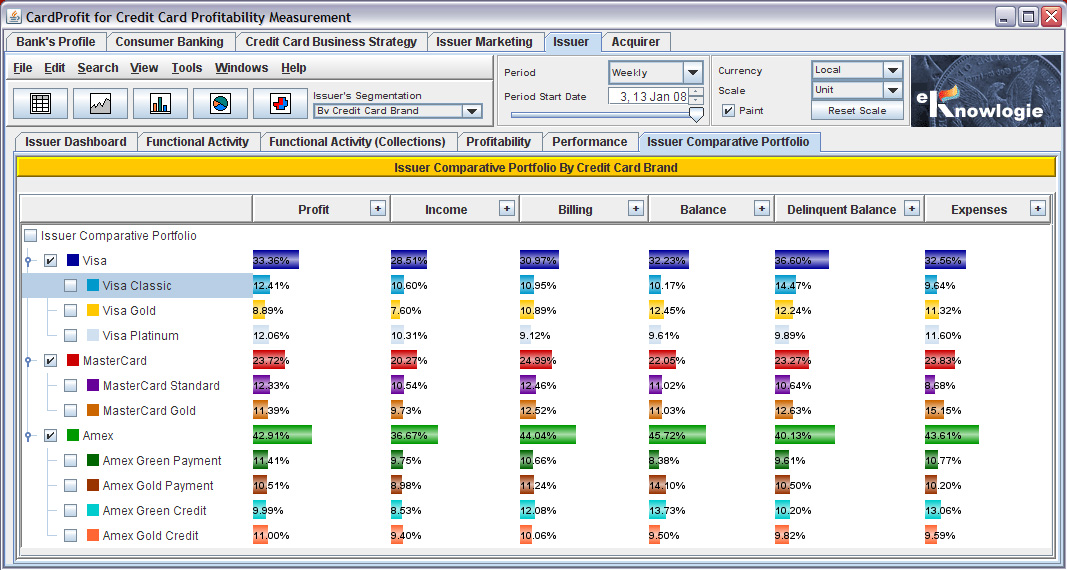

Issuer Portfolio

The following example shows a high-level view of the Issuer's consolidated portfolio segmented by

credit card brands. Notice that this is a comparative panel where the indicators are shown graphically

as percent bars. This same consolidated portfolio can be shown for any of the other Issuer segmentation

models, for example, by credit card type, by socioeconomic strata or by geographic region, etc.

1.5 Multidimensional Segmentations and Cross-Segmentations

A market, like the Issuer market, can be segmented according to any arbitrary criteria. Issuer can

be segmented by credit card product, by geographic regions, by cardholder transactional frequency ranges,

by credit limits, by credit limit utilization, by cardholder consumption habits (if available), by

promotional campaigns, by account acquisition harvests, etc. CardProfit can be used to model a given

segmentation in order to obtain a comparative profiling and differentiation of its segments in order to

improve performance and profitability. For example, we will know via unit indicators the ways a classic

product A might be under-performing a similar classic product B.

We can also cross these segmentations in order to obtain much more revealing insights that can further

improve performance. For example, if we cross products with geographic regions and cardholder transactional

ranges, we could discover that high transactor cardholders in a product Visa Gold in geographic region A are

outperforming the high transactors for the same product in socio-economically similar geographic region B.

Cross-segmentation can also allow us to differentiate delinquent cardholders according to the acquisition

harvest or marketing campaign to which they belong. This allows us to answer numerous questions which we

could not answer if we viewed every single segmentation separately. Then we can find out, for example,

what percent of travelling cardholders pay their balance in full or revolving or become delinquent and

further subdivide these segments by geographical regions. The example to the right shows a menu with

some possible Issuer segmentations. Only the segmentation by product and product brand is required for

Issuer. Other segmentations are optional.

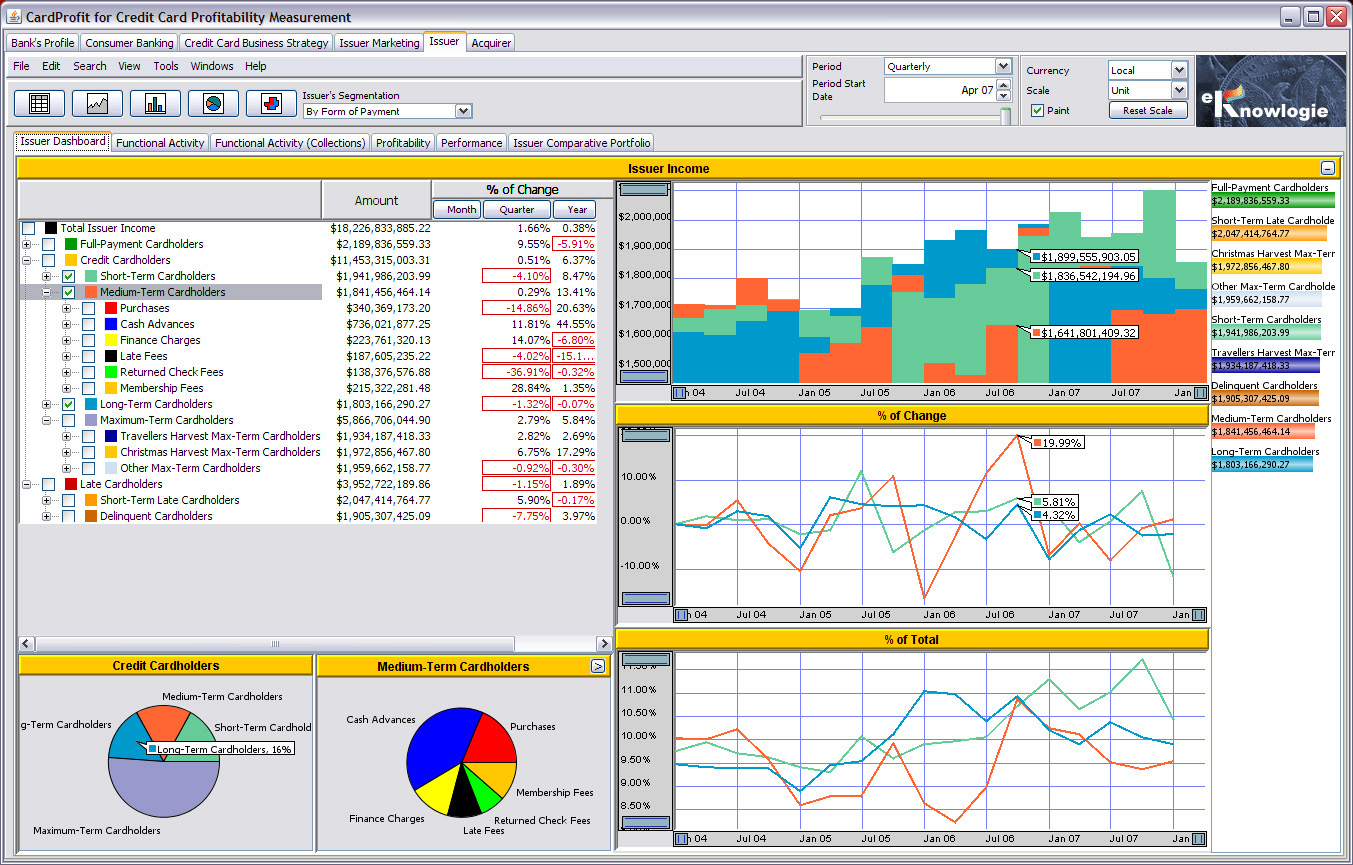

The following example shows the Issuer Income for the Forms of Payment segmentation. Notice how the

maximum-term cardholders segment (i.e. card holders that extend their credit by making only the minimum

monthly payments) is cross-referenced by the marketing campaign harvests. These market segmentations

allow us to analyze the campaigns' effectiveness in selecting new credit-oriented cardholders with low

incidence of delinquency.

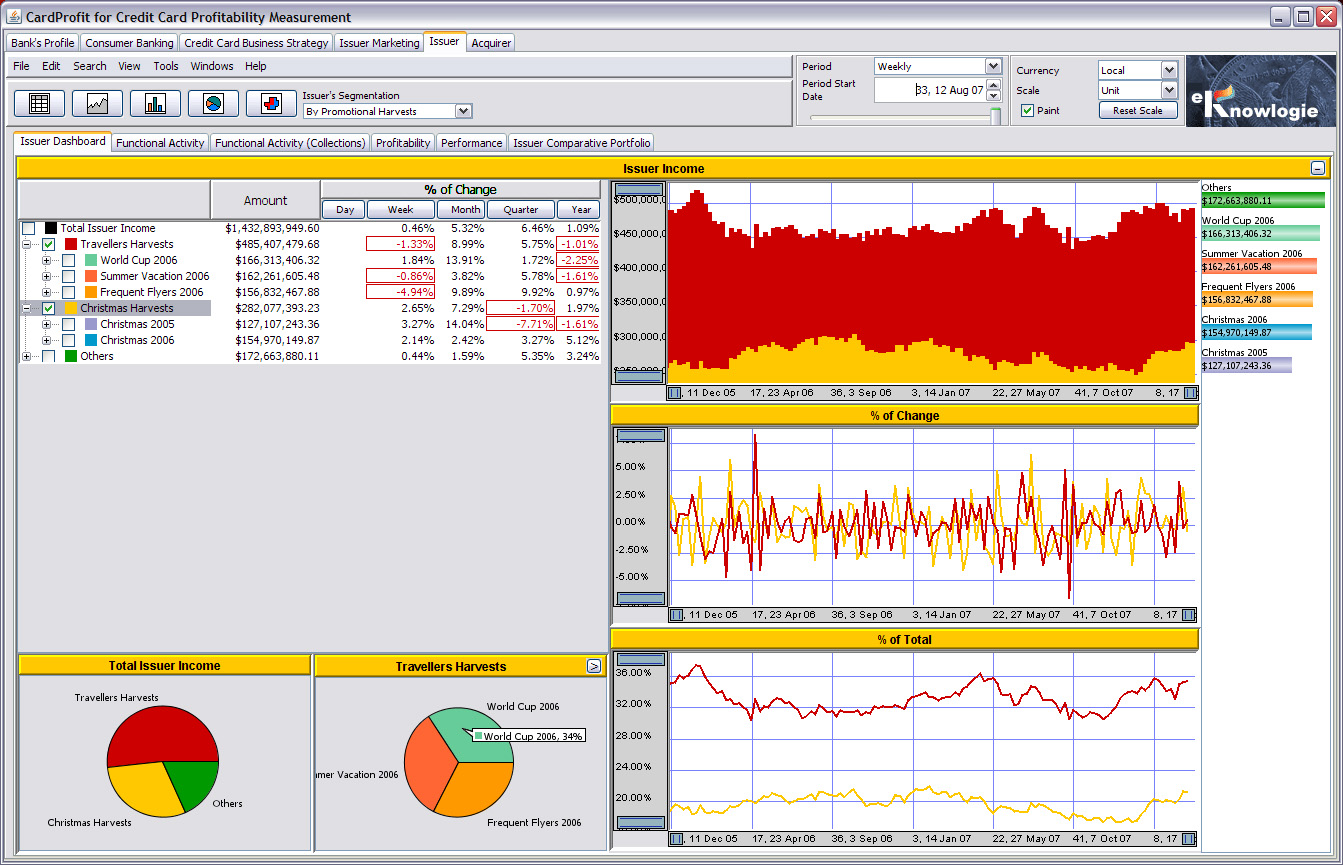

The example below shows the Issuer Income for the Marketing Campaign Harvests segmentation, using

a hierarchy that classifies them by type of promotional campaign.

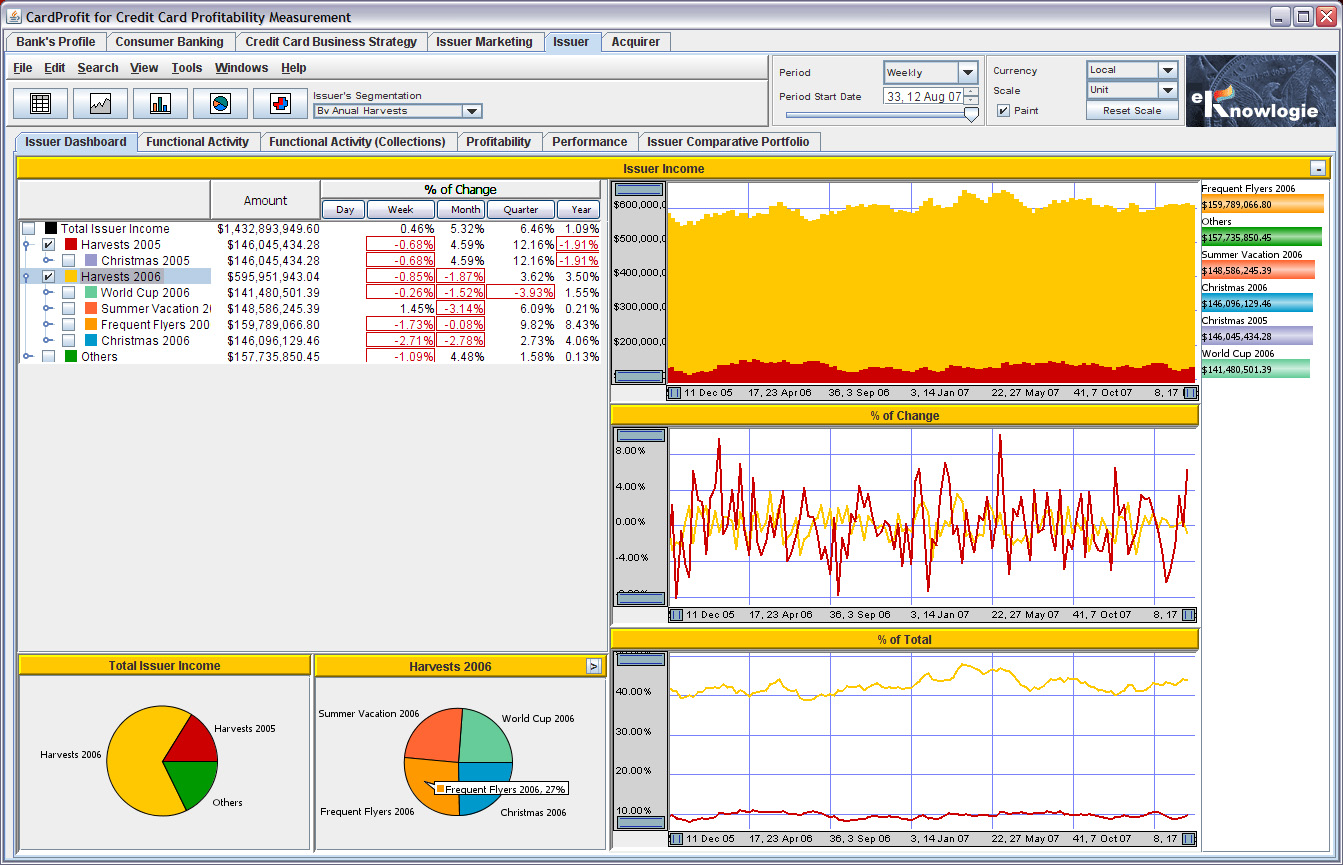

The following example shows the Issuer Income also for the same Marketing Campaign Harvests segmentation,

but this time using a hierarchy that classifies these segments according to their launch calendar periods. In

CardProfit, each segmentation can be classified according to multiple hierarchies.

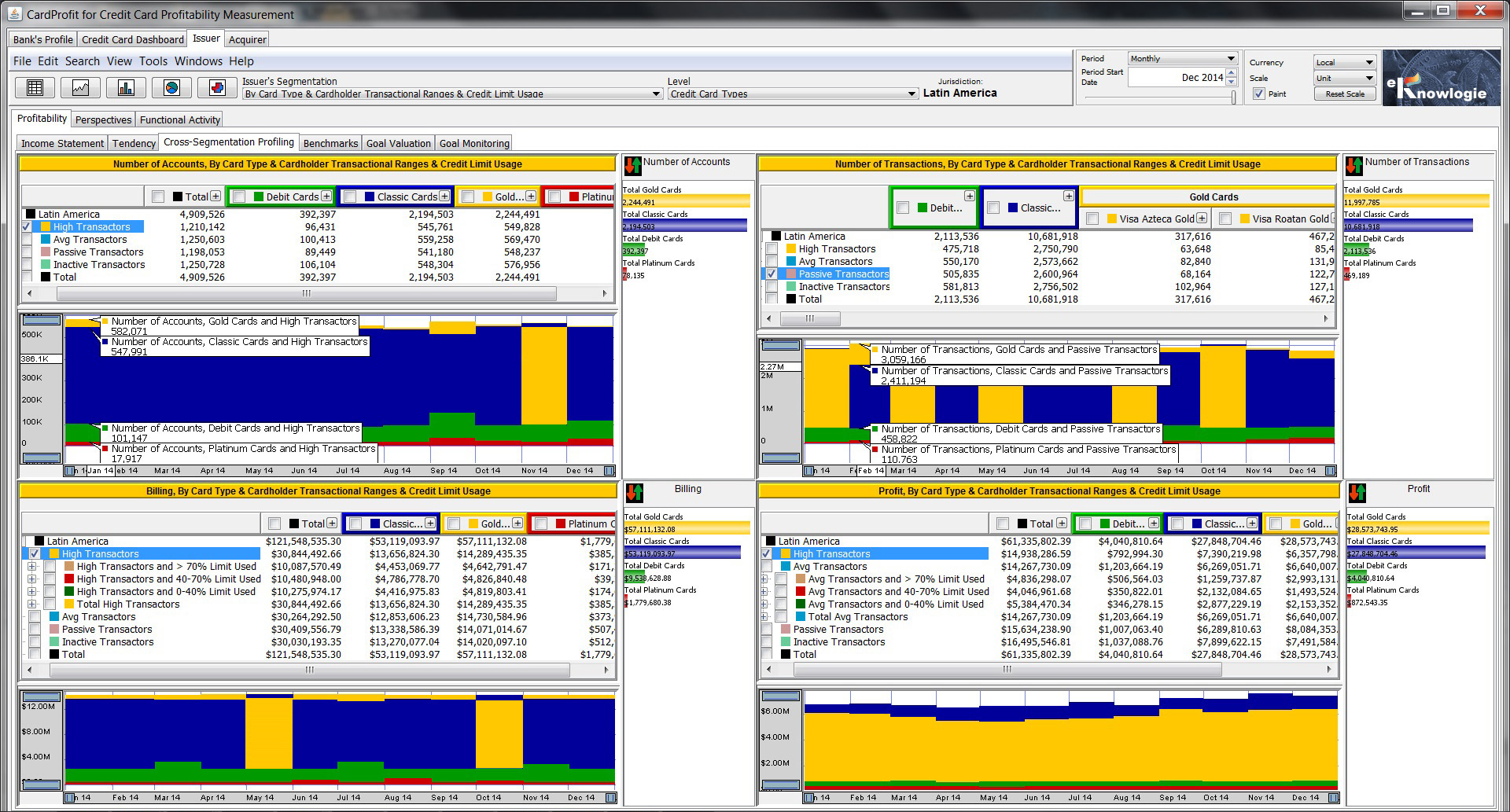

Intersecting or Crossing Credit Cards by Type with Cardholders by Transactional Frequency Ranges

Product types (e.g. classic, gold, platinum) can be profiled by the expected percentage of cardholders

in different transactional volume ranges (e.g. high transactors are cardholders who use the given card

for most of their transactions and they contribute the majority of the transactional volume for that given

product). The panel below shows the intersection or crossing of three segmentations, by product type,

by cardholder transactional ranges, and by credit limit usage. Then we can readily identify how effective

these products are in maximizing transactional volume according to their intended markets, and what cardholder

population redistributions are necessary in order to increase these volumes towards the expected profiles.

Because of the hierarchical nature of these tables, card type columns such as classic and gold can be

opened up so that specific products can be analyzed. Similarly, ranking bars can be shown for any level

in the intersection, e.g. by card types, by card types per cardholder transactional type, or by product

per cardholder transactional type. This hierarchical level management is conducive to the presentation

of detailed insights which illustrate the comparative essence of these product populations and leads to

informed recommendations and decision making. Again, figures in the example below are random and do not

reflect the realistic expectations of these segment intersections.

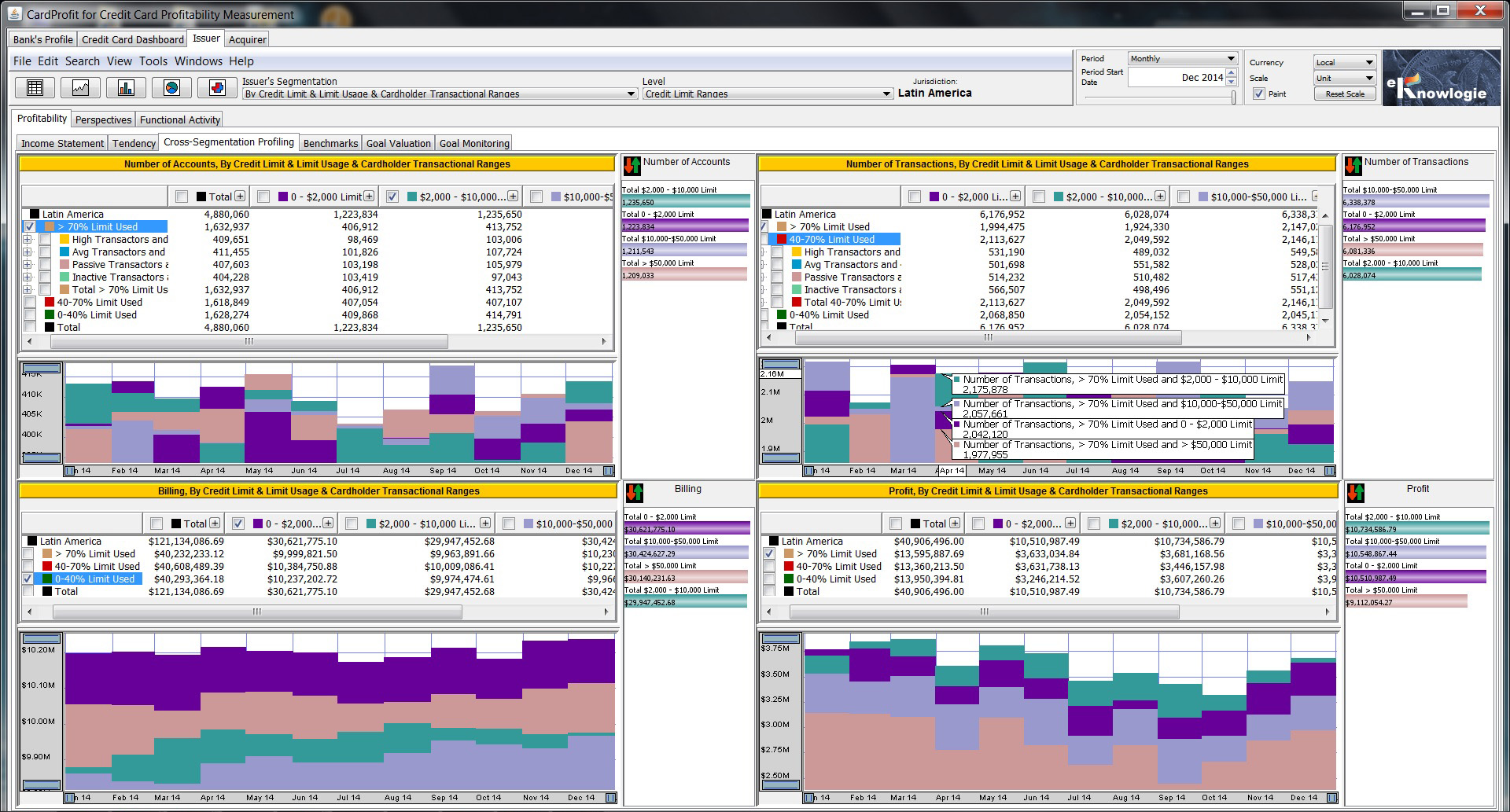

In addition, other market segmentations such as cardholders by balance and credit limit utilization

can be used to make these redistribution recommendations by identifying opportunities to retarget these

cardholder populations. The panel below shows the intersection or crossing of three segmentations,

by credit limit, by credit limit usage and by cardholder transactional ranges.

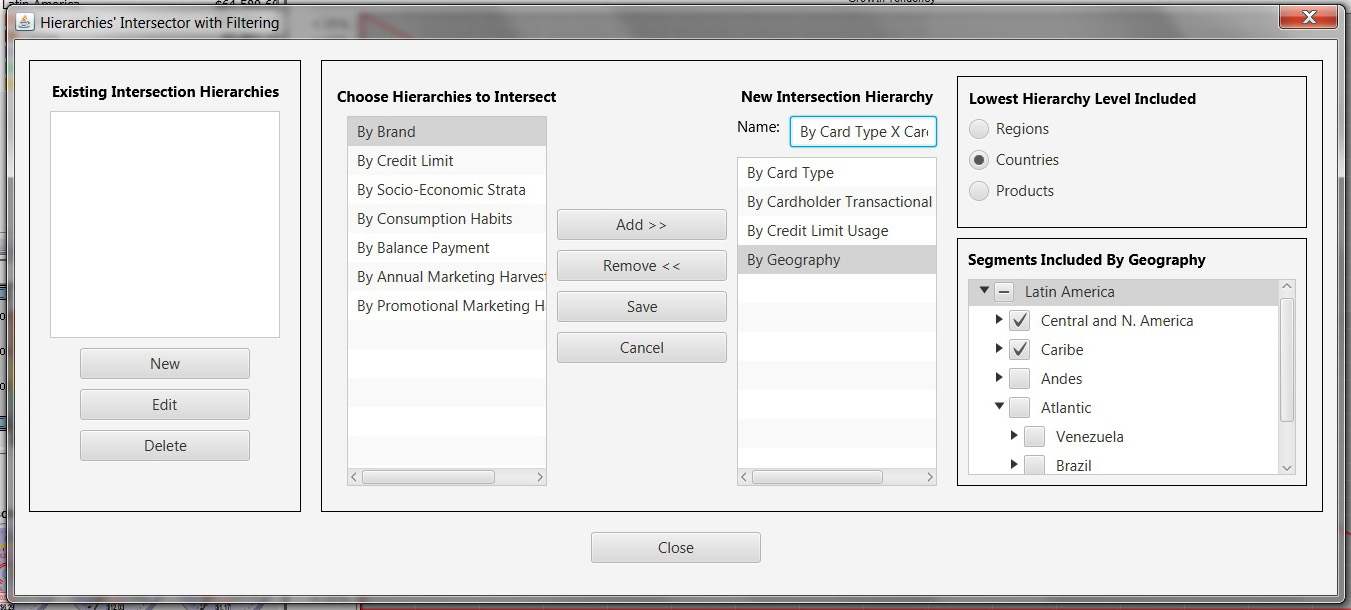

These segmentation crossings or intersections shown above are designed and configured by the user

interactively using the panel below. This panel allows the user to cross or intersect any number of

segmentations, in any order, and to specify the levels and segments that will be visible for each

segmentation. This is an example of the power of this technology.

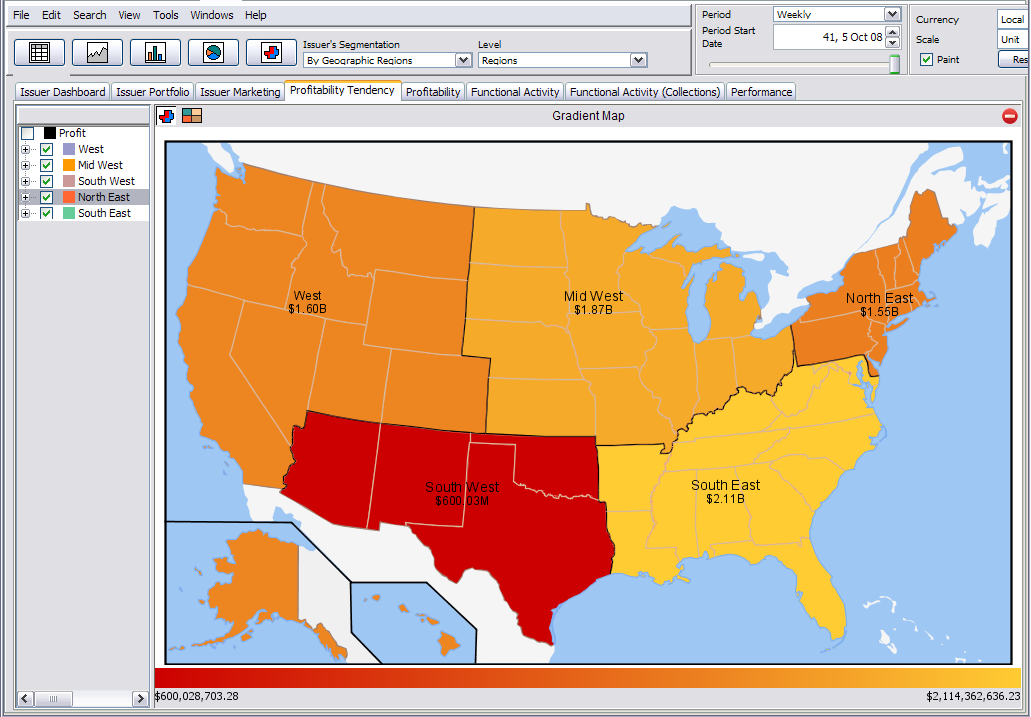

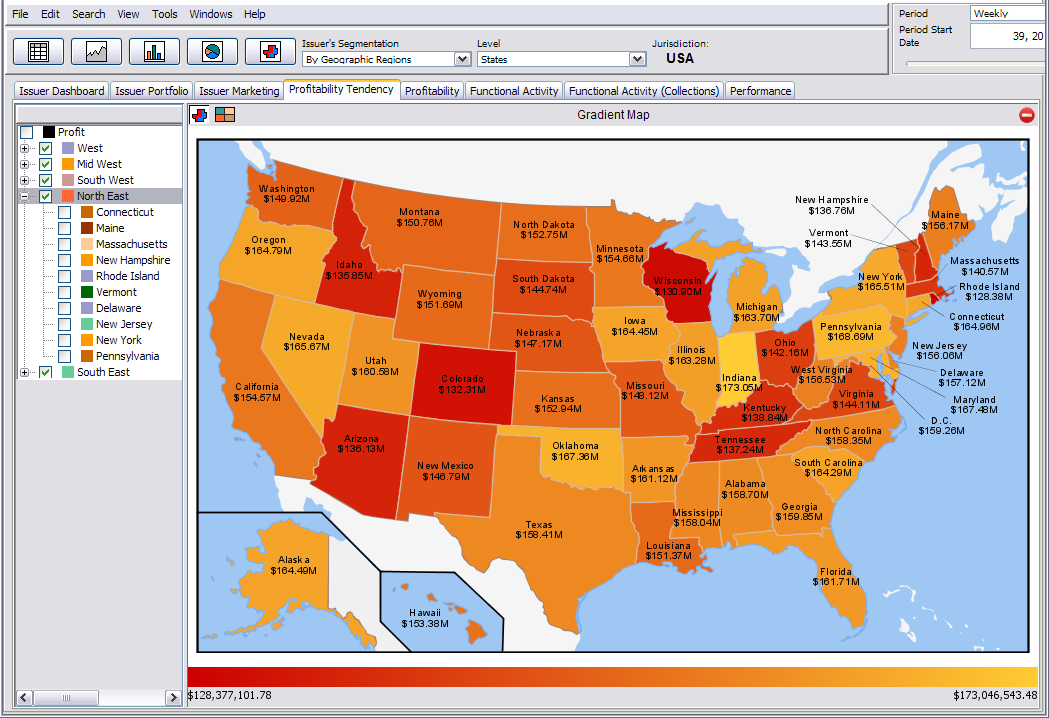

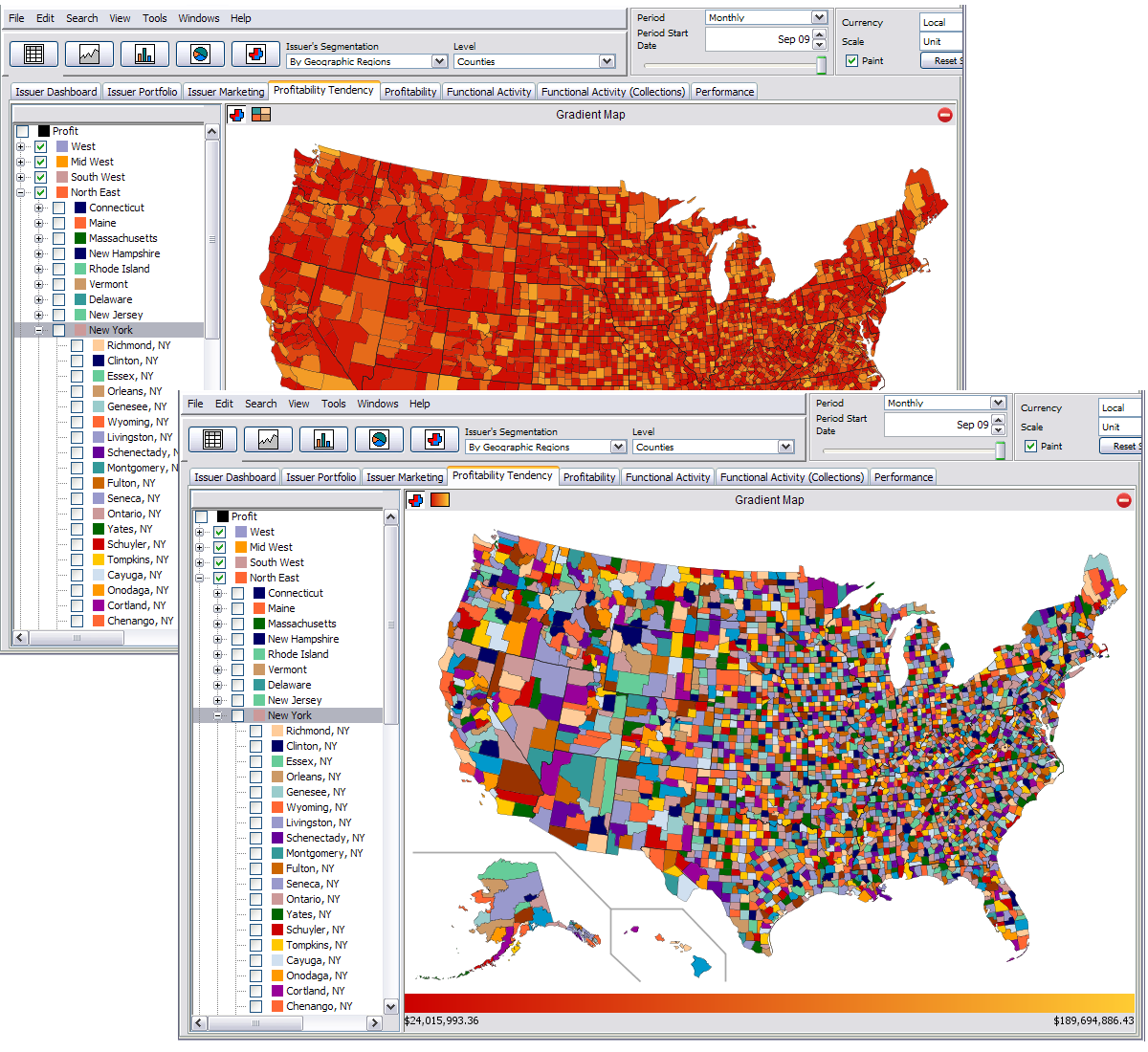

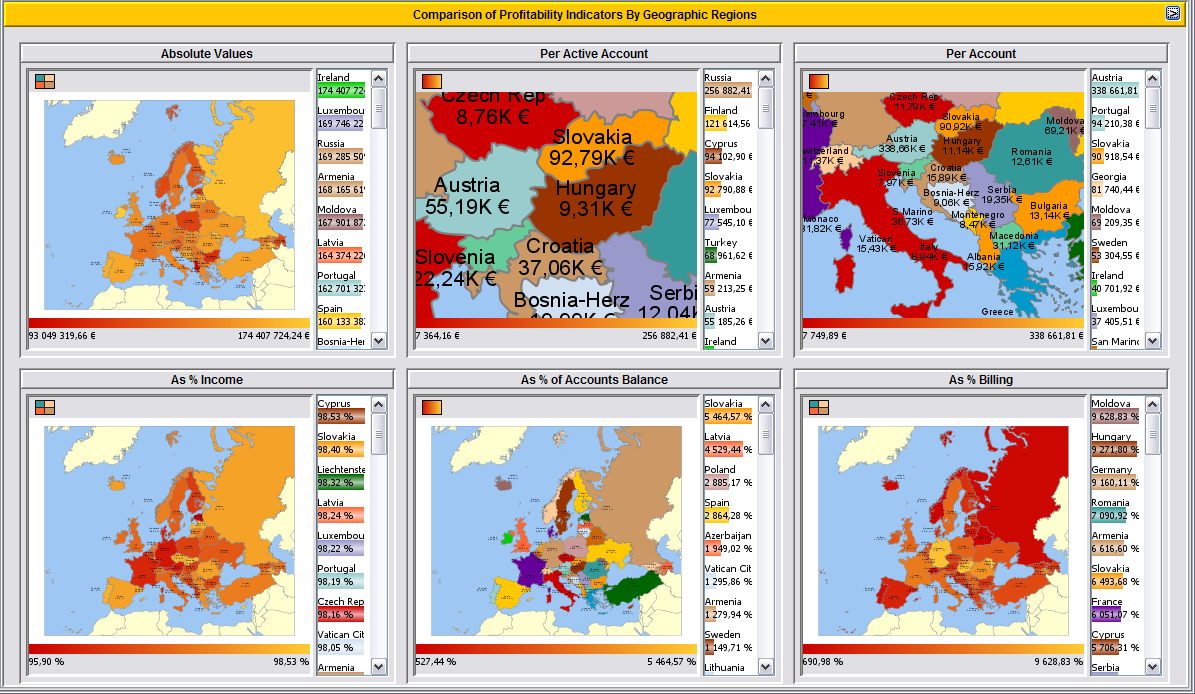

1.6 Geographic Visualization

The panels below show CardProfit's scalable choropleth maps (color-coded statistical maps) displaying

profitability indicators segmented geographically, where performance is visualized in a chromatic scale

from red (lowest performance) to yellow (highest performance). As shown below, geographical segmentations

can be visualized at their various hierarchical levels of detail.

Maps can also be used for color encodings other than gradient performance.

Profitability can be measured through a wide array of indicators as shown by the thumbnails in the following

example.

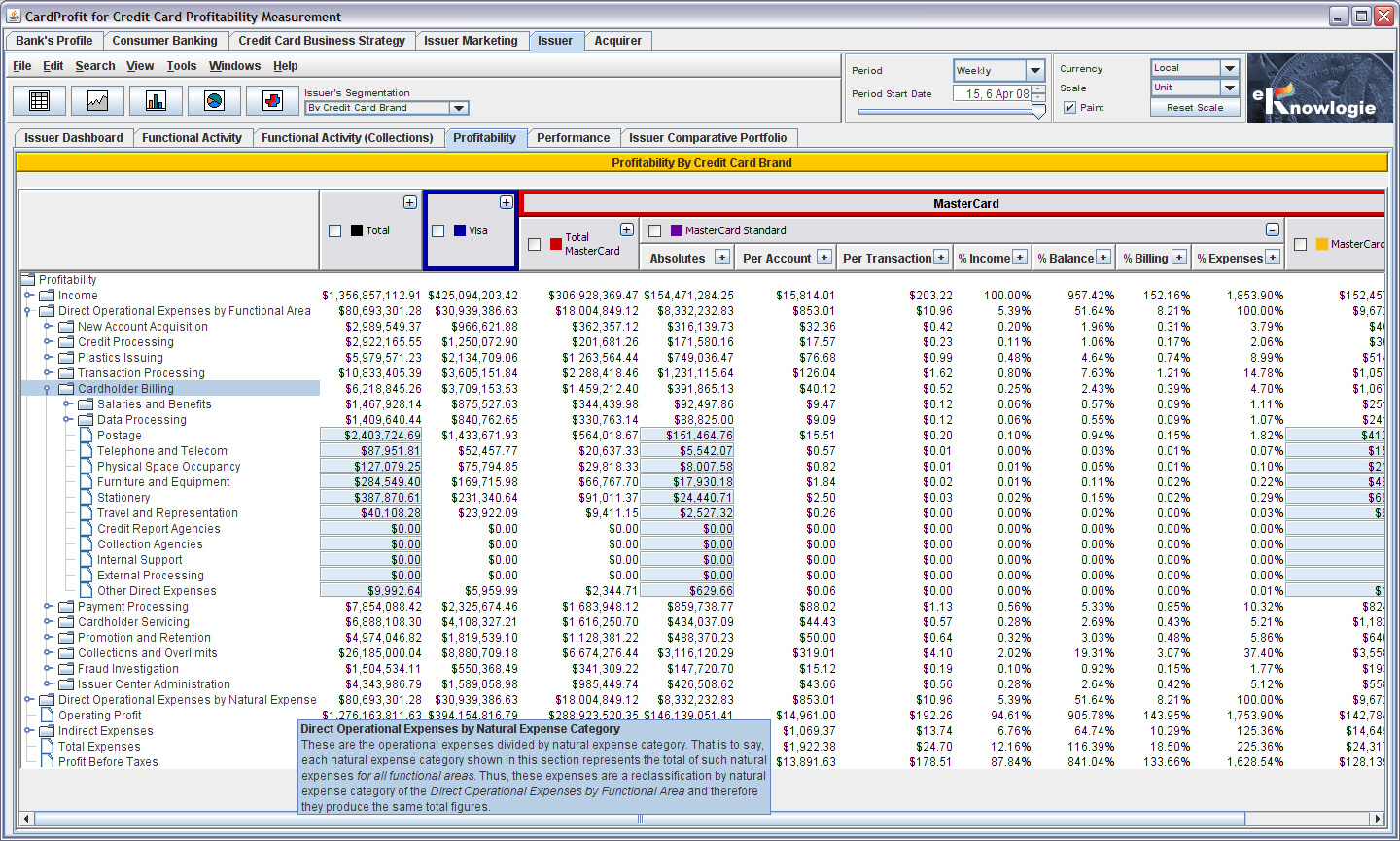

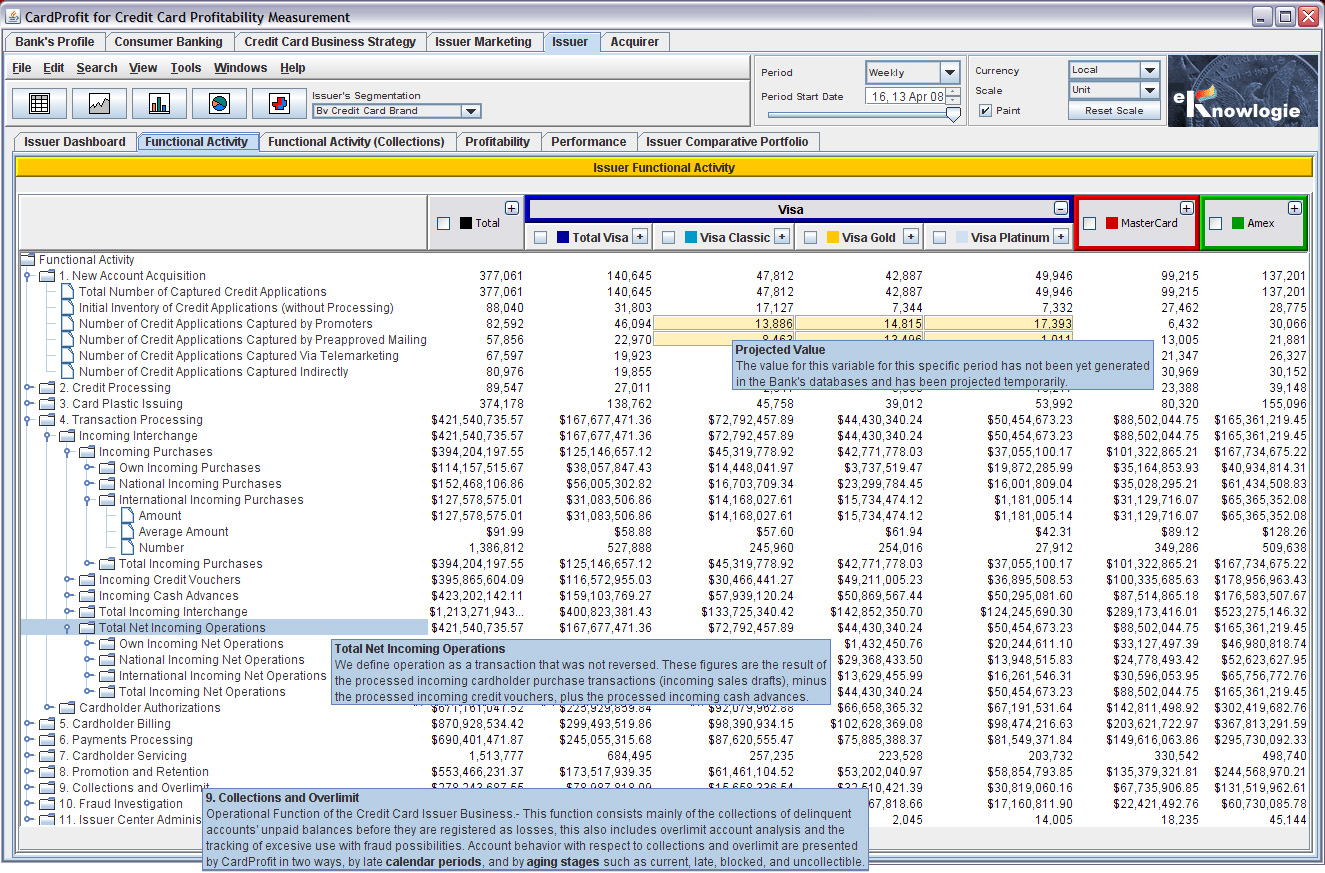

1.7 Issuer's Functional Activity

The following example shows in detail the indicators and variables of the Issuer's functional activity

segmented by credit card brand. Observe how the pop-up help window explains the "Collections and Overdraft"

category. These pop-up help windows exist not only to explain CardProfit functionality, but also to describe

each of the more than 1,100 indicators in the credit card business.

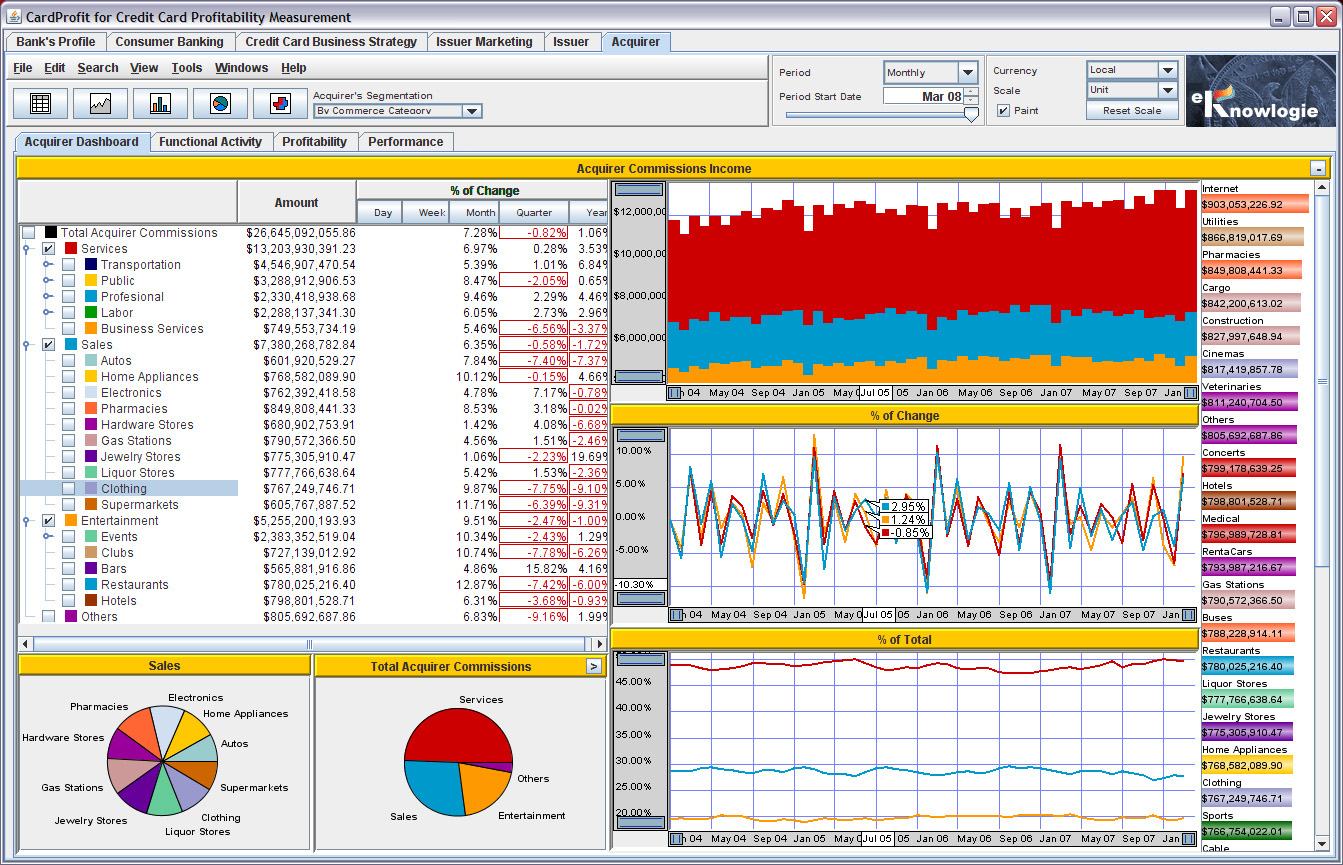

2 Acquirer

All the CardProfit functionality shown for Issuer is also applicable to Acquirer. The example

below shows the study page of the Acquirer Income, using a monthly period. Notice that

commerce categories are shown ranked by their income for the currently selected period.

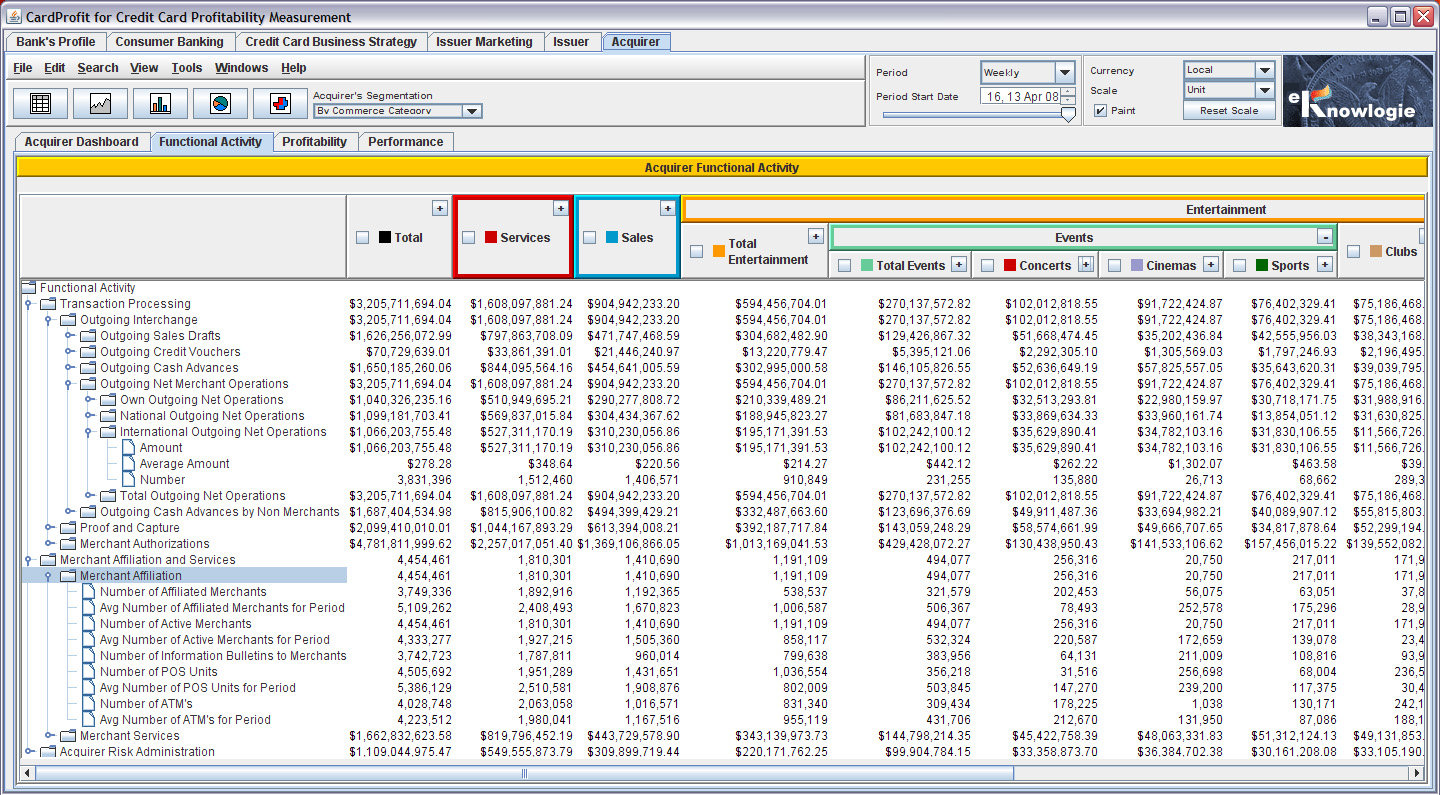

The example below shows the Acquirer business' functional and operational activity for each commerce

category.

3 Combined Issuer and Acquirer

With respect to the credit card Issuer and Acquirer lines of businesses, CardProfit manages more than 1,100

different primary variables which are specific to such businesses. CardProfit can be started effectively with

25 variables from each business line and gradually extended as justified by the added benefit of additional

measurements. CardProfit produces profitability and performance indicators by product or by any other

arbitrary user-defined market segments, as well as operational figures and indicators of natural expenses

and productivity specific to the functional areas of the Issuer and Acquirer businesses.

Each variable or unit indicator in the model can be visualized historically and through time periods

of any duration.CardProfit can be configured for any currency and world

region or locale. Although initially configured for English and Spanish, it can be easily configured

for any other language. eKnowlogie based its Issuer and Acquirer profitability models on the methodologies

developed by Global Payments, the banking consulting company with an exclusive emphasis on

credit card profitability and the most prominent in Latin America.

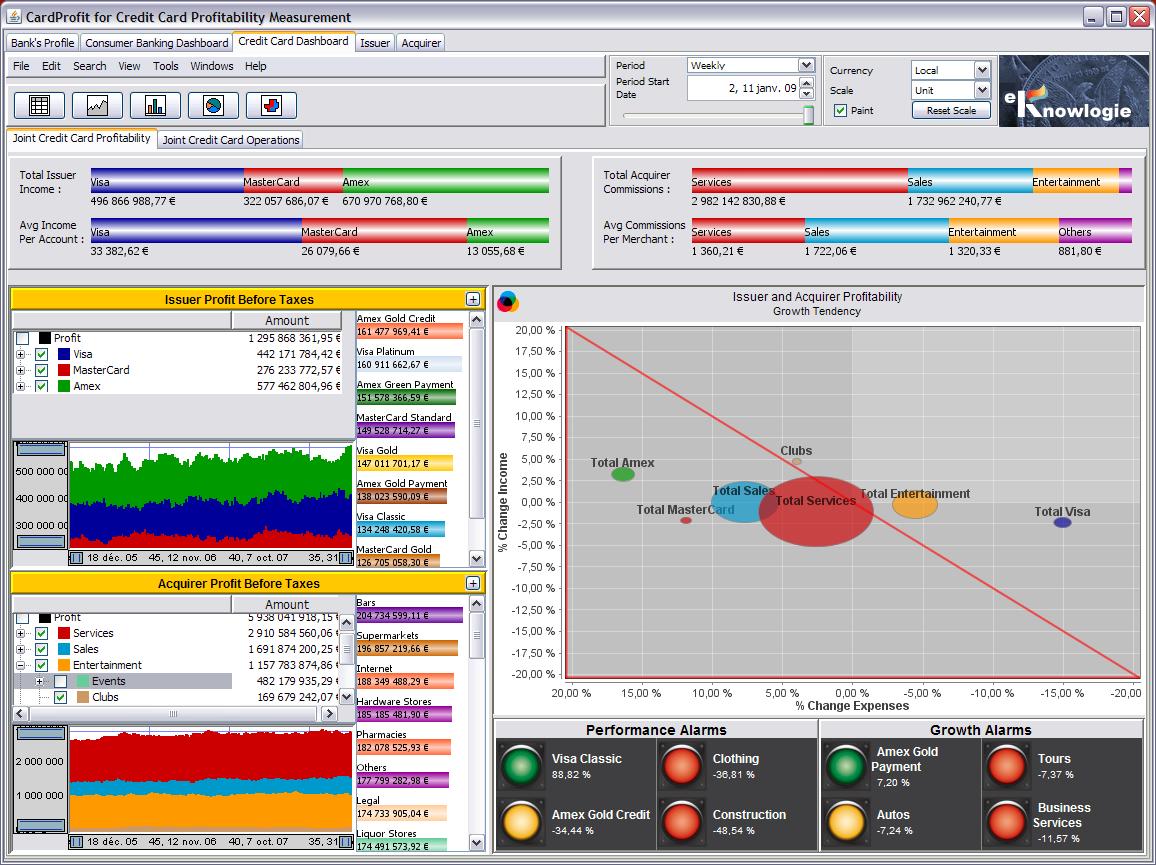

CardProfit offers consolidated combined perspectives for multiple lines of businesses. The following dashboard

shows combined Issuer and Acquirer profitability tendencies. The indicators represented in this bubble chart are

normalized, which permits the comparison of otherwise heterogeneous segments from both lines of businesses. Notice

that the values in these examples have been generated randomly and thus they are not realistic.

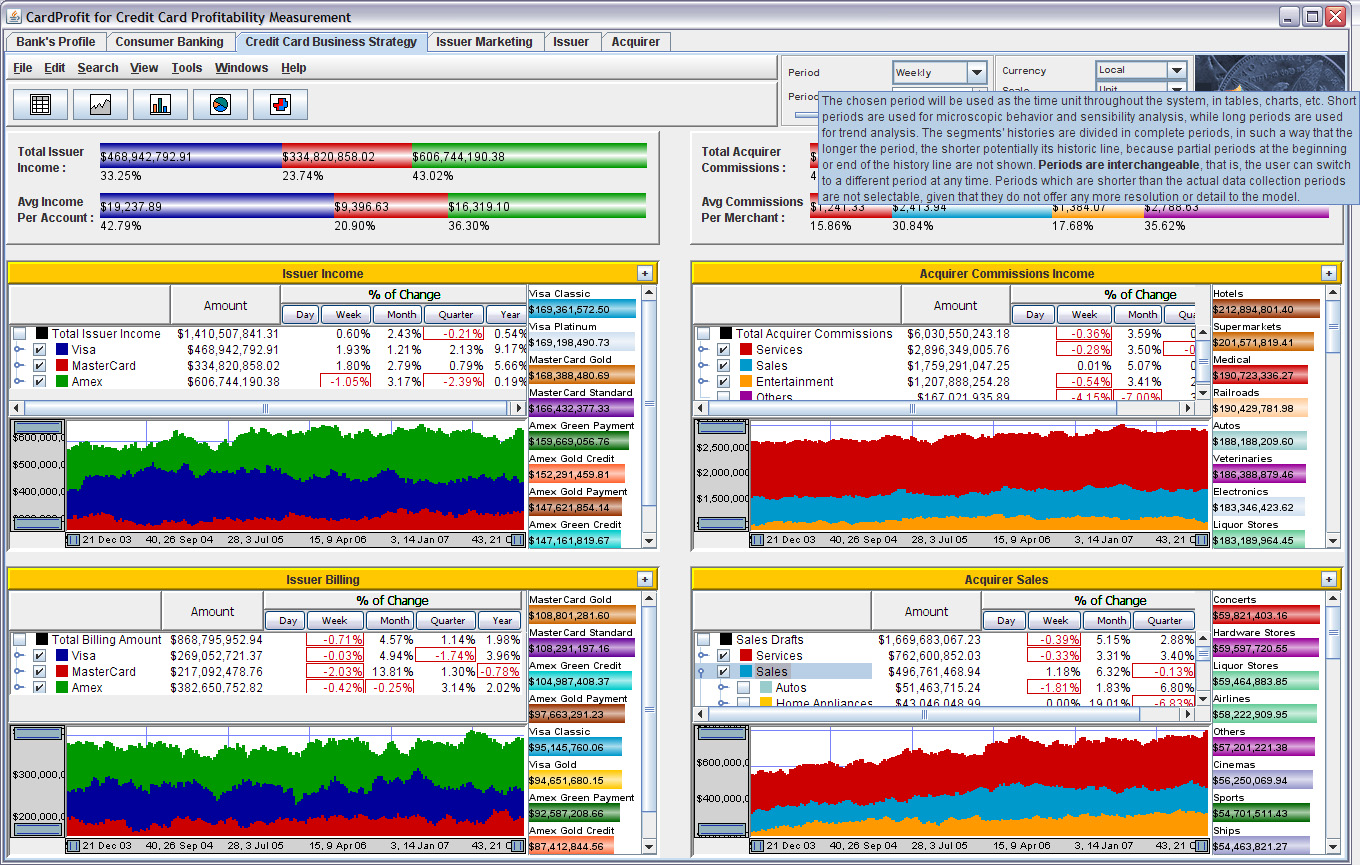

The following example shows another dashboard for the Issuer and Acquirer businesses. Each mini panel can be

maximized in order to visualize it in more detail and with additional instrumentation. Notice one of the many

pop-up help windows, which in this case describes the use of time periods throughout the application.

4 Client's Running Environment

CardProfit runs in 64 bit Windows 7 or 8 with preferred access to high-definition screens (1920 X 1080).

CardProfit makes use of multi-processor architectures for parallel execution of computation-intensive calculations.